64 / 84

64 / 84

The Economist

September 22nd 2018

Business 63

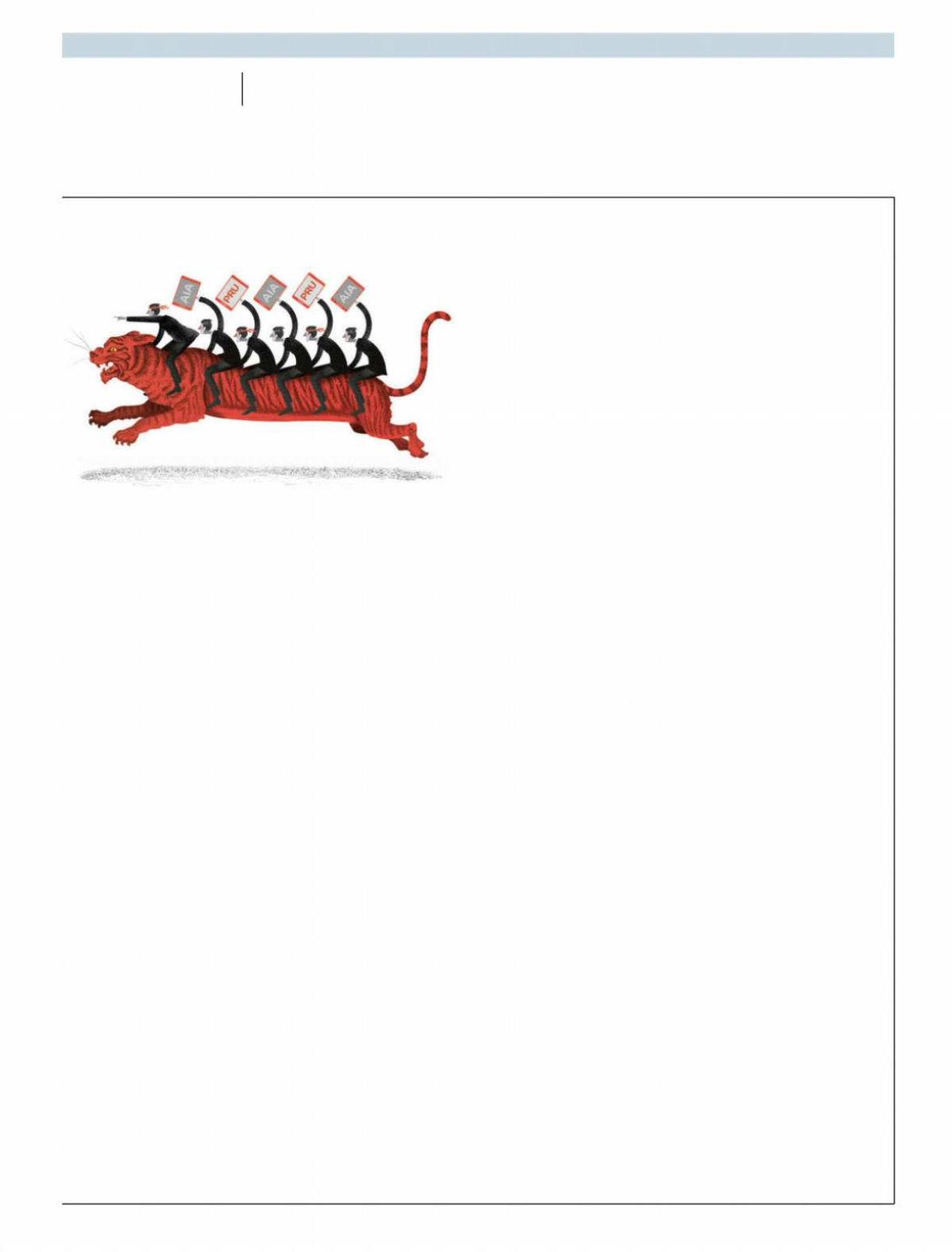

T

OYOTA, Unilever, Barclays, Amazon, Tata. There are 71,000

listed firms in the world, but only a few hundred that many

people knowat least a little about. Schumpeterwould like to pro-

pose two Asia-centric candidates:

AIA

and Prudential

PLC

. They

pass the key tests of relevance. They are big, with a combined

market value of $160bn. They are special, having grown profits

faster than two-thirds of listed companies over the past decade.

They have prospered against the odds, surviving wars, revolu-

tionary Shanghai, decolonisation and the 2008Wall Street crash.

And they illustrate a global trend: the rise of Asia as a mighty

force—perhaps eventually the dominant force—in global finance.

AIA

and Pru are specialists in getting Asians to save through

long-term insurance, typically life or health policies. They span

20 Asian countries, have over 60m customers and employ al-

most a million agents to sell their services. They are big investors

in local financial markets. And they are beneficiaries of powerful

trends. Asia’smiddle class is growingbut tends tohave its savings

stashed in cash. Welfare states do not yet offer an adequate safety

net if family members get ill or die. An obvious answer to this is

insurance, yet annual premiums are just 2.5% of

GDP

in emerging

Asia, comparedwith 5% inwestern Europe.

What is logical is not necessarily easy to achieve. Both firms

have had to go on odysseys.

AIA

was founded in Shanghai in1919

by an adventurer called Cornelius Vander Starr, and went on to

be folded into

AIG

, a huge, rogue American financial conglomer-

ate that got bailed out in 2008.

AIA

was spun out in 2010. Pruwas

founded in 1848 to serve the insurance needs of Britain’s middle

class. Its annual report from three decades ago mentions Asia

once. But in the 1990s it remembered that it had some operations

in the region that were remnants of colonial times and sent out

Mark Tucker, a young executive, to investigate. He ignited the

business, later became boss of Pru and then

AIA

, and is now

chairmanof

HSBC

—one of several star executives tohave been in-

volved. Tidjane Thiam, boss ofCredit Suisse, ran Pru in 2009-15.

Expanding life-insurance businesses is hard. You have to

spend cash up front onmarketing, agents and laying aside capital

reserves. The profits are spread over decades: 67% of the undis-

counted earnings from

AIA

’s book of policies will be realised

after 2038. In Asia each national market grows over time but in

volatile fashion, shrinking on average one year in every three.

Currencies gyrate. The industry is fragmented—there are at least

100 life firms across Asia. Someone is always starting a pricewar.

Both firms have found ways to cope. They are geographically

diversified. Each of India, Indonesia and Thailand have boomed

since 2008, only to slowdown. Between 2015 and 2017HongKong

tookoffasmainlandChinese flocked to sign up to policies in a lo-

cation with rule of law, but it has since hit saturation point. Now

parts of South-East Asia and mainland China are growing nicely

again. The firms’ armies ofagents are abarrier to entry that ishard

to replicate, and both companies avoid writing policies that re-

quiremarkets to soar in order to be profitable.

The result is that

AIA

and Pru’sAsian armhave increased their

operating profits at a compound rate of 13% and 18% respectively,

in dollar terms, since 2007. Two decades ago Asia represented 5%

of Pru’s market value; now it is about 50%.

AIA

is worth twice as

much as its former parent,

AIG

. The crumbs have become the big-

gest slice of the cake. For the global life industry Asian firms now

represent 49% of total market value, up from4% two decades ago.

China is a big part of the story. It has had fiascos, includingAn-

bang, a deal machine and patronage vehiclemasquerading as an

insurance firm, that failed in February. But there are serious com-

panies, too. PingAn is themost valuable life firm in theworld and

is admired for its use of data. China Life ranks third.

AIA

owns

100% of a mainland operation and Prudential has 50% of a joint

venture with

CITIC

, a state-run conglomerate. These bets have

achieved critical mass, delivering 18% of the new business writ-

ten so far this year for

AIA

and 11% for Pru Asia. The two firms are

set to join a tiny elite ofmultinational financial firms that derive a

significant share of their global profits frommainland China.

One risk to them is technology. For now, customers still like

dealing with a human (armed with an iPad) when signing com-

plex policies. But startups accessing customers through their

phones could make agents obsolete. Colm Kelly, an analyst at

UBS

, has surveyed 800 agents inAsia, and halfof them think that

digital distribution is a “big threat”. The management of

AIA

and

Pru need to take this more seriously. Another danger is an eco-

nomic crisis in Asia, spurred by trade wars or a sell-off in emerg-

ing markets. Insurers are inherently opaque. Still, in the 2008-09

downturn

AIA

and Pru Asia avoided big underwriting-and-in-

vesting banana skins, while newsales dipped only a little.

Deal or no deal

Instead the big testmay be consolidation. China is easing its rules

on foreign ownership, which will prompt a reshuffle among the

long tail of 26 other foreign life firms that have a presence there.

Ping An and China Life may seek to buy a presence abroad. Con-

tinental Europe’s two giants,

AXA

and Allianz, both say that they

eschewbig deals, but have spare cash, half an eye onAsia and 20-

year records of empire-building through acquisitions.

For

AIA

, the danger is that it overpays for small deals or faces a

big new competitor. For Prudential the risk is it faces an opportu-

nistic takeover bid. It is the smaller of the two, with a less mature

book of business that throws off less cash. In 2019 it will spin off

its British arm. The idea is to lose this baggage so that Pru gets a

racier valuation, but the unintended effectmay be tomake it a sit-

ting duck. Ping An has reportedly been sniffing around its Asian

business. Pru’s board should resist any bid and stiffen its share-

holders’ resolve. Both it and

AIA

belong at the forefront of a new

generation ofAsian financial multinationals.

7

Metamorphosis

TwoAsian financial giants deserve to be betterknown

Schumpeter