78 / 100

78 / 100

66 Finance and economics

The Economist

May 5th 2018

1

2

The number of people visiting Bank of

America branches has declined from a

peak of1mweekly a couple of years ago to

850,000, even as the volume of transac-

tions has increased. A quarter of all depos-

its are now done using a cheque-photo-

graphing feature on smartphones.

Finally, however, Mr Moynihan can re-

turn to thoughts of expansion. The bank

has announced that it will start to open

new branches once more. There will be

fewer teller windows and more side-of-

fices where staff can sell investments and

loans. It is also trying to create a bridge be-

tween its retail branches and its wealth-

management and investment-banking ac-

tivities. It wants to drum up business from

midsized companies that would prefer to

issue securities through the investment

bank, rather than take a loan, and from in-

dividuals who would like investment op-

tions alongside their bank accounts. It has

built a new electronic platform, Merrill

Edge. That should help it compete with Fi-

delity and Charles Schwab, and provide

new clients for Merrill’s brokers, now re-

branded financial advisers.

None ofthis is all that dramatic. But that

is intentional. After the trauma of the fi-

nancial crisis, any abrupt or daring change

ofdirection by a bigAmerican bankwould

probably be blocked by regulators. For

nowand some time to come, the twinaims

will be to keep improving operational effi-

ciency and avoid disaster. Mr Moynihan

has done well enough at both that, when

the time comes to replace him, there

should be plenty ofwilling candidates.

7

A

FTER just 18 days as Deutsche Bank’s

chief executive, Christian Sewing had

two tasks to perform on April 26th. The

easy one, inherited from his ousted prede-

cessor, John Cryan, was to report predict-

ably glum first-quarter results. Net profit

dropped by 79%, year on year, to only

€120m ($147m). Harder was indicating

where he might lead Germany’s troubled

leading lender. The rough answer is: back

towards Europe, and away from any aspi-

ration to be a global investment bank.

Mr Sewing intends to concentrate more

on raising finance and managing pay-

ments and currencies for big European

companies, and less on America and Asia.

He plans to cut the small swaps-repurchas-

ing business in America and to focus the

buying and selling of shares for hedge

funds andotherinvestors on themost prof-

itable clients. By 2021 corporate and invest-

ment banking’s share of total revenues

will be trimmed to 50%, from54% last year.

As a result, Mr Sewing said, earnings

should becomemore stable.

So far, says Andrew Coombs of Citi-

group, Mr Sewing has supplied “more

questions than answers”. He thundered

about cost-cutting. Yet he still aims only to

keep operating costs below €23bn this

year—a target raised by €1bn in February.

Longer-term guidance for costs, revenue,

assets and leverage is still to come. Mr

Coombs worries that restructuring may

cost farmore thanDeutsche is allowing for.

So the leverage ratio (a gauge of capital

strength), which at 3.7% is well below the

figures for its peers, may fall in the short

run. Withdrawal from those trading busi-

nesses should lift it, but because contracts

can last a long time, thismay take awhile.

As well as its corporate and investment

bank, Deutsche has Germany’s biggest re-

tail bank (plus banks in Italy and Spain)

and an asset manager,

DWS

. It thus seems

to be settling for being a universal bank

with its centre of gravity in Europe. This is

far from the course of the 1990s and 2000s,

when Deutsche and other European ad-

venturers tookonWall Street.

Such a model can be made to pay.

France’s

BNP

Paribas also combines retail

banking, in Belgium, Italy and Luxem-

bourg as well as at home, with a division

serving corporations and institutional in-

vestors that has a strong European flavour.

Granted, the French bank, which is due to

report first-quarter results on May 4th, re-

turned an unspectacular 8.9% on equity

last year (it hopes for 10%-plus by 2020). Its

stockmarket worth is 15% below the book

value of its assets. But for Deutsche, that’s

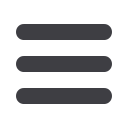

dreamland (see chart).

There are important differences. France

has a fewbig banks; Germany lots of small

ones. Though bigger by assets than Deut-

sche,

BNP

Paribas is a smaller investment

bank. Coalition, a research firm, ranks it

sixth in Europe andDeutsche second, with

Americans taking the other top slots.

Comewhatmay, Europeans’ glory days

are gone. Tighter capital rules since the fi-

nancial crisis, notes Alastair Ryan of Bank

of America Merrill Lynch, have hit them

harder than American banks. The Ameri-

cans’ vast balance-sheets and huge domes-

tic market give them scale that Europeans,

with smaller markets and minuscule rates

andmargins, cannot match.

The Americans were also quicker than

Europeans to shape up after the crisis.

Europeans have had to choose new mod-

els. Switzerland’s

UBS

tacked from invest-

ment banking towards wealth manage-

ment; Credit Suisse may have pivoted to

Asia just in time; Barclays styles itself as a

transatlantic bank;

BNP

Paribas was never

a true swashbuckler anyway.

Even by European standards, Deutsche

was slow. As late as 2015 it believed that as

others retrenched it would be the “last

man standing” and make a killing when

business pickedup. Did itwake up too late?

Over to you, Mr Sewing.

7

Reshaping Deutsche Bank

Shrink to fit

Europeanuniversal banks can succeed.

But canDeutsche Bank?

Modesty pays

Source: Bloomberg

Ratio of share price to net book value per share

0 0.5 1.0 1.5 2.0

JPMorgan Chase

Morgan Stanley

UBS

Goldman Sachs

Bank of America

Credit Suisse

Citigroup

BNP Paribas

Barclays

Société Générale

Deutsche Bank

P

OPULAR concern about free trade with

China has focused on the loss ofmanu-

facturing jobs in America and Europe.

Policymakers have an additional worry:

that China’s rise is hurting innovation in

theWest. This fear is among the small set of

issues that unites American Democrats

and Republicans. In 2016 Barack Obama’s

commerce secretary said that China’s

state-driven economy would weaken the

world’s innovation ecosystem. Donald

Trump’s advisers allege that China makes

it harder for foreign firms to invest in inno-

vation by squeezing their returns. Mr

Trade and innovation

China chill

SHANGHAI

Reports of the death ofAmerican

innovation are exaggerated

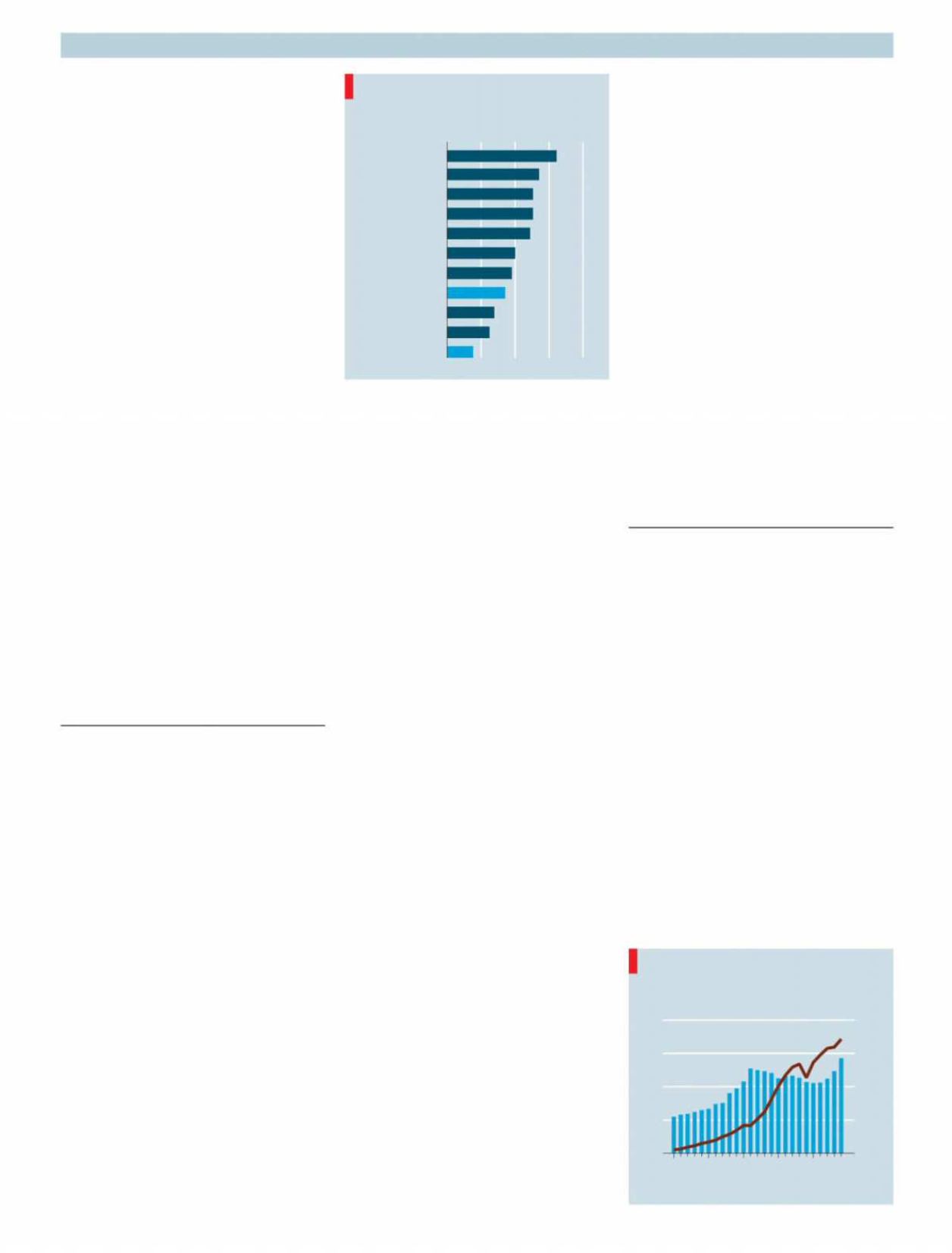

Patently obvious

Sources: IMF; CEIC

*Set of patents covering a single

invention in more than one country

0

20

40

60

80

0

100

200

300

400

1990 95 2000 05 10 14

United States, patent

families

*

, ’000

US goods-trade deficit

with China, $bn

РЕЛИЗ ПОДГОТОВИЛА ГРУППА "What's News"

VK.COM/WSNWS