79 / 100

79 / 100

The Economist

May 5th 2018

Finance and economics 67

2

Trump’s trade team was expected to raise

this complaint, among others, with Chi-

nese officials during talks inBeijing onMay

3rdand4th, as

The Economist

went topress.

There is one problem. Data suggest that

competition with China has coincided

withmore innovation inAmerica, not less.

The relationship between competition

and innovation is complex, even before

considering trade with China. Economists

agree that the right competitive landscape

fosters innovation. But theydisagree about

what exactly that landscape looks like.

More competition might prod companies

to try harder to develop new products in

the hope of gaining market share. Alterna-

tively, if competition is cut-throat, profits

might evaporate to the point that compa-

nies have little incentive to take risks.

The fear is that China generates the

wrong kind of competition and stunts the

good kind. Businesspeople elsewhere

worry that when the Chinese government

decides to fund this or that industry, invest-

ment soars and margins collapse. Over-

capacity in steel was caused in part by Chi-

nese investment in steel processing;

semiconductor firms think their industry

might be next. At the same time, argues

Robert Lighthizer, the

US

Trade Representa-

tive, foreign companies that beat their Chi-

nese competitors are not adequately re-

warded because China presses them to

transfer their intellectual property.

The two main academic papers on this

question looked at the years around Chi-

na’s accession to the World Trade Organi-

sation in 2001. Far from settling the matter,

they were contradictory. Economists

studying European companies found that

competition from Chinese imports both

caused firms to improve their technology

and led to a shift in jobs to the most ad-

vanced firms. They concluded that 15% of

the upgrading of technology in Europe be-

tween 2000 and 2007 could be attributed

to the increase in imports from China. But

economists examining the impact on

America argued that, on the contrary, Chi-

nese competition had led companies to

spend less on research as profits fell. They

calculated that imports from China ex-

plained 40% of a slowdown in American

patenting between 1999 and 2007, com-

paredwith the preceding decade.

The

IMF

has now weighed in with

more recent figures. Its conclusion is rather

more cheerful, at least for those who think

a tradewarwith China is a rotten idea. In a

report published in April the fund showed

that, following an extended period of de-

cline, high-quality patents granted to

American companies had risen sharply

between 2010 and 2014. It also pointed to a

big increase in American spending on re-

search and development during the same

years—even as America’s trade deficit with

China rocketed (see chart on previous

page). The growth in patents was more

sluggish in Europe and Japan. But both pat-

ents and research spending soared in

South Korea, the country most directly ex-

posed to manufacturing competition from

China.

A separate

IMF

working paper late last

year unpicked some of what is happening

inAmerica. Competition fromChinese im-

ports has caused research spending to be

reallocatedwithin certain industries, away

from also-rans and towards the most pro-

ductive and profitable firms. At the same

time, many researchers left manufacturing

industries and moved into service sectors

such as data-processing and finance. Both

results are consistent with an American

economy that is playing to its strengths.

The

IMF

’s analysts concluded that Chinese

imports were not a threat to innovation in

America, after all, and that policymakers

could take a deep breath. No loud inhaling

sounds have yet been reported from the

White House.

7

Returns to education

Smart investment

W

HICHhas provided a better return

in recent decades: America’s stock-

market or education? The latter, accord-

ing to a research reviewbyGeorge Psa-

charopoulos andHarry Patrinos for the

World Bank. The two economists looked

at1,120 studies, across139 countries, and

came upwith an annual average “rate of

return”—actually a pay premium, the

increase in hourly earnings froman extra

year of schooling—of 8.8%. The analogy is

inexact, but for comparison America’s

stockmarket returned an annual 5.6%

over the past 50 years.

Their figure excludes social gains, such

as lowermortality rates associatedwith

greater education. The premium is higher

for girls and for primary education. It is

also higher in poor countries, presum-

ably because the smaller the share of

educated people, the higher the pay they

can command. The same reasoning

suggests that the return should have

dwindled as educational attainment

rose. Instead, it has stayed strong, espe-

cially for higher education (see chart).

Some researchers have posited that

technological advances have displaced

some skilledworkers, who have then in

turn displaced less-skilled ones, leaving

their relative positions in the pecking

order—and thus the return to their extra

education—little changed. Mr Psacharo-

poulos andMr Patrinos aremore san-

guine. They think theworld iswitnessing

a “race between education and tech-

nology”. A rising number of degree-

holders has tended to push returns

down, but rising demand for higher-level

skills, driven by the speed of technologi-

cal change, hasworked in the opposite

direction. Technology seems to have

beenwinning.

Rising returns increase the incentive

to invest in education. Governments and

individuals seem to be responding. Pub-

lic spending on education as a share of

GDP

is growing; private education, both

at school and tertiary level, is booming.

The beneficiaries are peoplewho have

access to education, either because they

live in rich, well-governed countries or

because they can afford to pay privately

for it. Rising returns, saysMr Patrinos,

signal to individuals to invest more. But

they alsomean that anyonewho does

not will fall further behind. “Eitherway,

the conclusion is the same: invest now.”

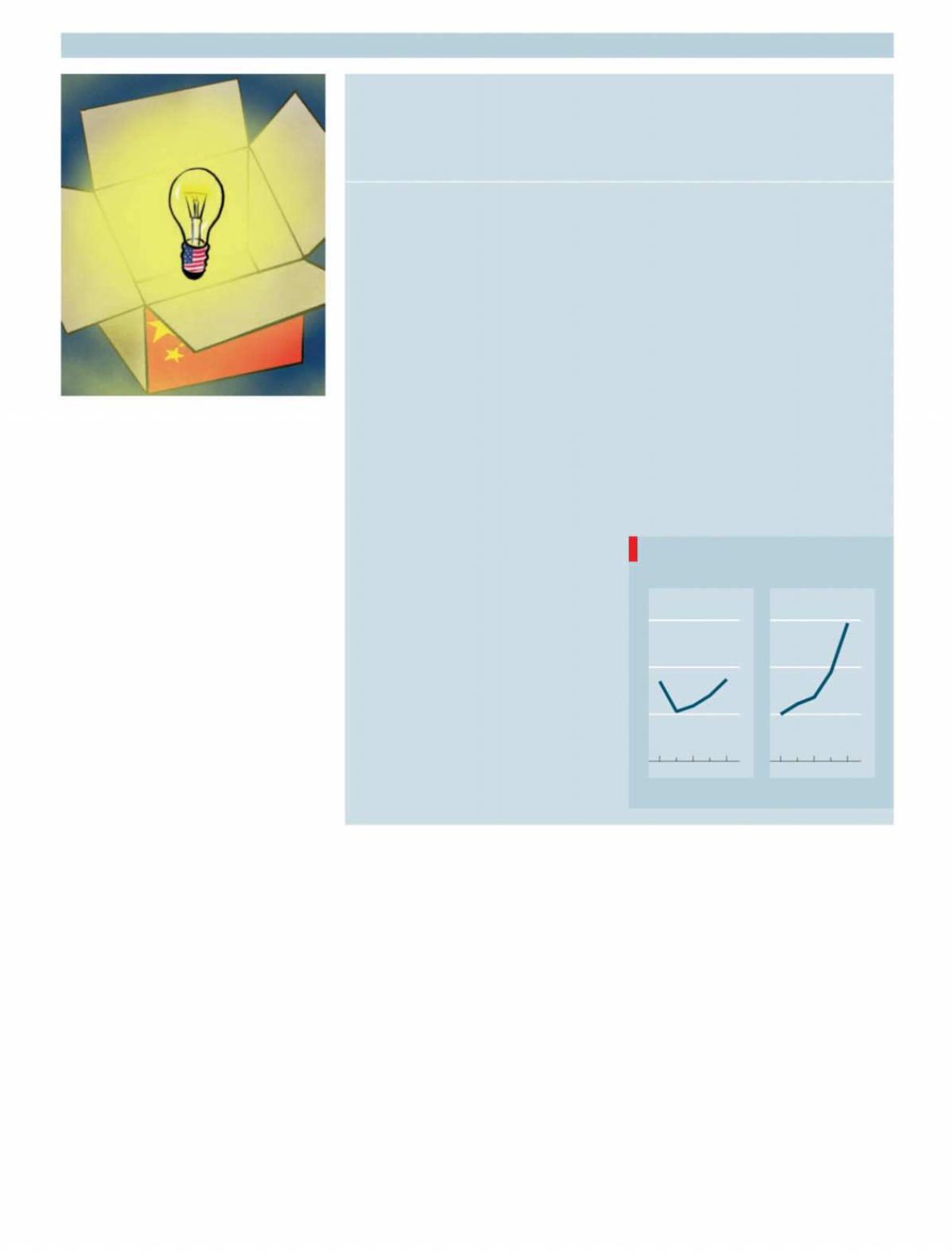

Even thoughmore people are doing it, studying still pays off

Honour roll

Source: George Psacharopoulos and

Harry Patrinos, World Bank

Global higher education

Rate of return

Annualised, %

Enrolment

As % of population

0

10

20

30

1970 90 2010

0

10

20

30

1970 90 2010

РЕЛИЗ ПОДГОТОВИЛА ГРУППА "What's News"

VK.COM/WSNWS