11 / 96

11 / 96

The Economist

April 14th 2018

Leaders 11

1

2

Some argue that a bombing campaign would merely pro-

long Syria’s war, which Mr Assad, regrettably, has all but won.

Rebels control only a few pockets of territory in the north and

south and are largely cut offfrom international support. Deter-

rence has already failed, say others, and hitting the dictator

againmight provoke a response fromRussia, which has threat-

ened to shoot downAmericanmissiles andfire at their launch-

ers. More risks come with the man in charge of the mission,

President Donald Trump. His Syria policy is scandalously in-

consistent (see Middle East and Africa section). Only last

month he indicated he would withdraw American troops,

saying “Let the other people take care of it now.”

The costs of inaction

These are serious concerns. But they do not justify inaction,

which would embolden Mr Assad to commit more atrocities.

In the past, a failure to act has had precisely this effect. Barack

Obama called the use of chemical weapons a “red line”. Yet

when Mr Assad used Sarin nerve gas to kill 1,400 civilians in

Ghouta in 2013, Mr Obama did too little, settling for a disarma-

ment deal that Mr Assad quickly broke. Mild punishments

have not worked, either. WhenMr Assad used Sarin again last

year,Mr Trump launched 59 cruisemissiles at a Syrian air base,

and then stopped. That did not deter the attackonDouma.

Mr Assad’s next target is rebel-held Idlib, where thousands

of civilians are hunkered down—and where new chemical

massacres are likely if nothing is done. Hitting him hard

enough to prevent such horror runs the riskofprovoking Vlad-

imir Putin, Russia’s leader and Mr Assad’s protector. Care

should therefore be taken to avoid killing Russians. Existing

“deconfliction” arrangements should be used to give Russian

commanders warning of imminent attacks, and thus a chance

to get their men out of the way. America should make it clear

that itwishes to avoid a direct confrontationwith another nuc-

lear power. Such a campaignwill require nerve and precision.

Evenwith both, it is not without risks.

Yet it is the least bad option. Syria has made a mockery of

the

UN

’s Chemical Weapons Convention, which Russia and

MrAssadhimselfhave signed. Ifsuchagreements are tobe tak-

en seriously, they must be enforced. Alas, the

UN

cannot per-

form this task as long as Russia wields its veto at the Security

Council. So the burden falls on countries that believe that the

rules-based international order isworth upholding.

Mr Trump champions such rules only when it suits him.

Nonetheless, he is right to argue that Mr Assad should pay a

“big price” for his crimes, and he deserves credit for calling out

Iran and Russia for backing Syria’s tyrant. If he means what he

says, he will not be alone. Countries as diverse as France and

Saudi Arabia are urging that Mr Assad be held accountable.

Punishing the use of chemical weapons will not end the

suffering in Syria, or unseat Mr Assad. But if the taboo on

chemical weapons is allowed to fade away, other despots will

be tempted to use them, too. And war, already vile, will be-

come evenmore so.

7

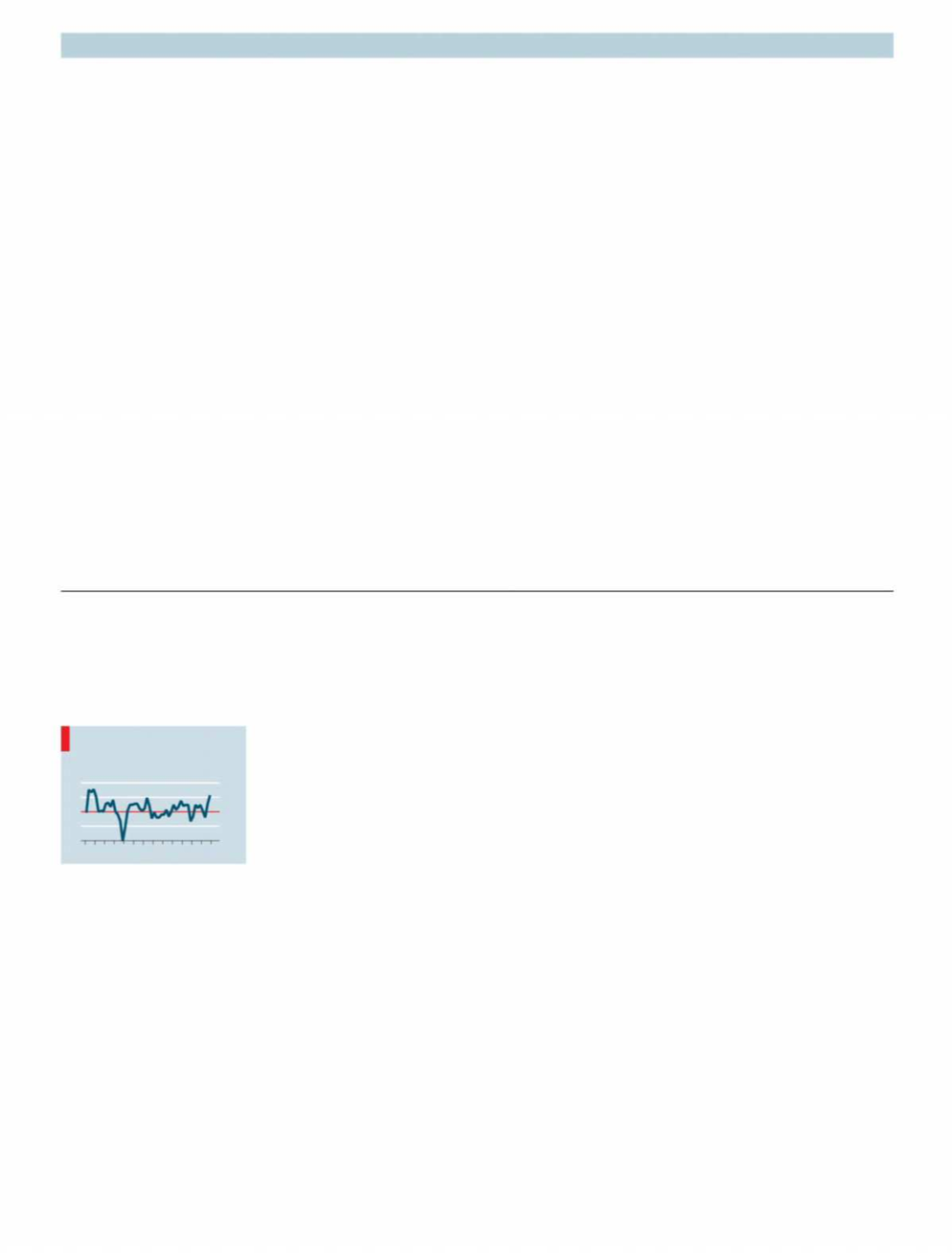

L

OW productivity growth has

plagued Britain’s economy

since the financial crisis. From

2010 to 2016 output per hour

grew, on average, by just 0.2% a

year, down from 2.5% between

1950 and 2007. In the

G

7 group

of rich countries, only Italy has

doneworse. Productivitydrives a country’s living standards in

the long term. It is a relief, then, that the stagnation may at last

be coming to an end. In the second half of 2017 productivity

grewat an annual rate of 3.4%, the fastest growth since 2005.

Accelerating productivity is the latest, and most important,

piece of good news on Britain’s economy. Capital spending is

improving. As a share of

GDP

, total investment is a percentage

point above its average since the crisis. Foreign firms are readi-

ly investing. A tenth of global mergers and acquisitions an-

nounced so far in 2018 have involved a British target. Wage

growth is picking up in nominal terms and, with inflation fall-

ing, real wagesmay soon start to growagain.

The strength of Britain’s labourmarket stands out. America

may have a lower official unemployment rate, but nearly a

fifth of people there aged between 25 and 54 are not even look-

ing for work, meaning they are not counted in the figures. Not

so in Britain, where the employment rate for this age group is

84%, among the highest of large economies.

Inevitably in a country still riven by the referendum deci-

sion to leave the European Union, Britain’s economic perfor-

mance is analysed through the prismofBrexit. Those in favour

of leaving the

EU

gleefully recall predictions, made by the Trea-

sury and others, of a collapse in confidence after the referen-

dum, and then a recession. Not only have those forecasts

proved wrong but, some Brexiteers say, Brexit may actually be

helping the economy. On their view, productivity is rising be-

cause falling net migration from Europe has led to a tighter la-

bourmarket, spurring firms to findways to domorewith less.

Too soon to celebrate

Not so fast. The reasons for the rise in productivity are not yet

clear (see Britain section). But there are two ways in which the

recent economic newsmust be put into perspective.

The first is that the aftermathofthe referendumhas coincid-

ed with a broad, sustained rise in global growth. Against that

backdrop, it is not surprising that Britain’s economy has per-

formed better than anticipated. It has nonetheless slowed. The

economygrewbyonly1.4% in the year to the endof2017, down

from 2% a year earlier. And it has slipped sharply relative to

others. Not long ago Britain had the fastest growth in the

G

7

group of rich countries. Now it has the slowest. Comparing

Britain’s growthwith that of theworld economy, one estimate

puts the running cost of Brexit at 1.3% of

GDP

, or £300m

($426m) a week. Had the global economic cycle not turned in

2017, some of the more blood-curdling forecasts made before

the referendummight not have looked quite so silly.

Brexit and the economy

Brittle Britain

Britain, output per hour

% change on previous six months

Annualised

2005

10

15 17

6

3

0

3

6

+

–

Productivity is rising at last. On its current course, Brexit threatens to undermine those gains